How the Cash Advance Strategies Work

MABLE Holdings employs two cash advance strategies to generate income.

They are:

- HICCAs- Health Insurance Commission Cash Advances

- MCAs- Merchant Cash Advances

Each one will be described in detail below.

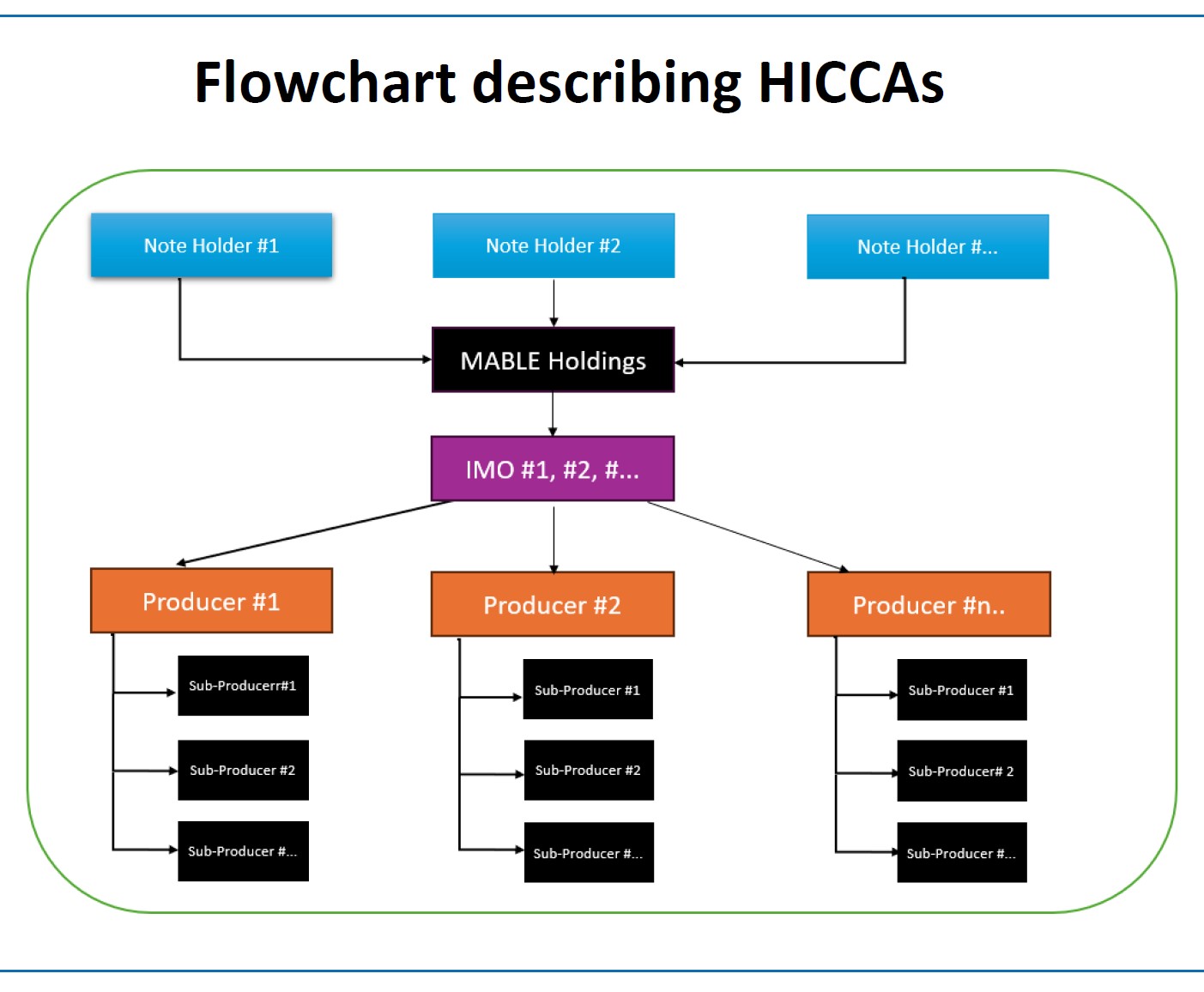

Health Insurance Commission Cash Advances

Health Insurance Commission Cash Advances (“HICCAs”) involve advancing funds against future commissions to licensed health insurance agents (“Producers” and “Sub-Producers”) who have sold defined health benefit plans (“Products”) offered by insurance companies (“Insurance Companies”) to individuals and households (“Members”).

Insurance Companies typically distribute their Products through Independent Marketing Organizations (“IMOs”), which oversee networks of approved Producers and Sub-Producers. These Products generally offer limited benefit health coverage—such as doctor visits, prescription services, and routine care—and are often designed to supplement high-deductible insurance plans. As a result, they are commonly marketed to younger and generally healthier individuals seeking more affordable coverage alternatives.

IMOs and/or third-party administrators ("TPA") are responsible for collecting monthly premiums from Members, typically through recurring credit card payments, and remitting the appropriate amounts to the Insurance Companies. To provide an incentive to Producers and Sub-Producers, IMOs may offer upfront payments representing a portion of the commissions expected to be earned over time.

To facilitate these upfront commission payments, firms such as MABLE Holdings provide cash advances to IMOs. In return, MABLE Holdings is entitled to receive the commission stream generated from Member payments until the advance is repaid, together with ongoing monthly service fees calculated on a per Member per month (PMPM) basis.

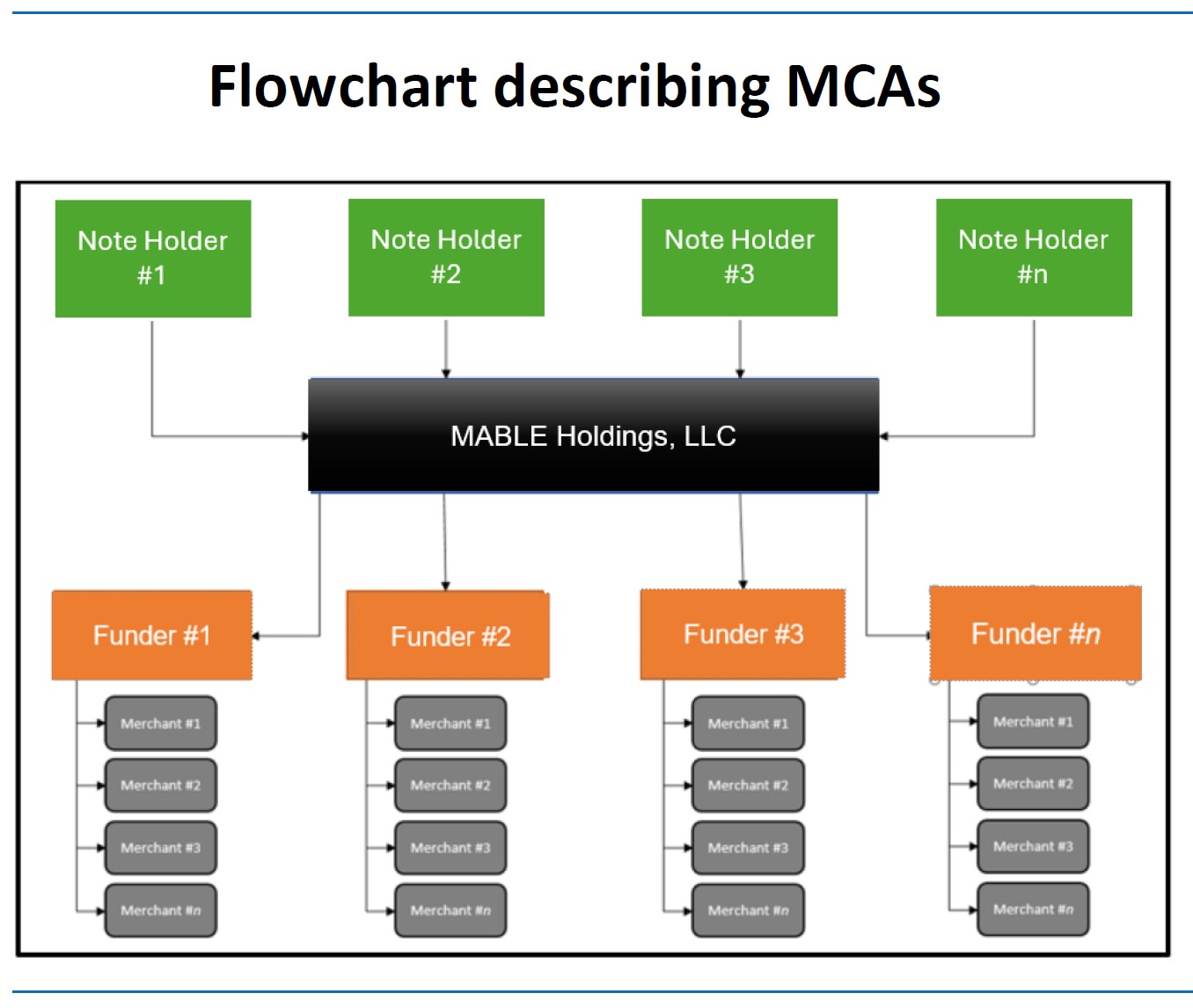

Merchant Cash Advances

A Merchant Cash Advance (“MCA”) is a financial transaction in which a Funder purchases a specified portion of a merchant’s future receivables in exchange for providing the merchant with an upfront lump sum of capital. MCAs are structured as purchases of future revenue rather than loans. Small and medium-sized businesses often encounter challenges in obtaining timely financing through traditional banking channels, which may involve lengthy approval processes, extensive documentation, and strict underwriting requirements. MCAs are designed to address these limitations by offering expedited access to short-term working capital. Businesses may choose MCAs as a funding alternative for several reasons, including:

- Speed of Funding: MCA transactions can often be approved and funded within a short timeframe, in some cases as quickly as 24 hours, whereas traditional bank financing may take weeks or months to complete.

- Reduced Documentation Requirements: Compared to commercial bank loans, MCAs generally require less documentation, simplifying the application and approval process.

- No Collateral Requirement: MCAs are typically unsecured and do not require the merchant to pledge specific assets as collateral, unlike many traditional loan products.

- No Equity Dilution: Merchants retain full ownership of their business, as MCAs do not involve the issuance of equity interests.

- Shorter Duration: MCAs are generally structured as short-term transactions, often with expected repayment periods ranging from approximately four to ten month.

Want to learn more?

Zoom meeting is for informational purposes only.

No securities will be offered or sold during this discussion.

No investment decision should be made based solely on this discussion.